The rule everyone is arguing about

In 2026 the consistency rule became the most-argued rule in prop trading. One firm raised its cap from 30% to 50%. Another removed it from its funded accounts. A third built its whole pitch around not having one. One prop firm's founder, in a 2026 interview, called the rule "a payout trap."

The argument is loud because the rule sits on top of money. It decides when a trader gets paid. But the question of whether the rule is fair skips the more useful one for an operator: what is the rule for, and does it do the job?

This piece is for operators who run a challenge-and-funding model and treat the consistency rule as a risk setting. It is a proxy for something the setting cannot deliver. We covered the broader version of this gap in the prop firm retention playbook; this is the single-rule deep dive.

What the consistency rule is

The consistency rule caps the share of total profit that can come from a single trading day. The math is one line: best-day profit divided by total profit, as a percentage. If a trader's best day is $3,500 of an $11,000 total, that is 32%. Most firms set the cap somewhere between 20% and 50%.

What happens if you breach the consistency rule?

In most cases, nothing terminal. A breach does not fail the account. It delays the payout. The trader has to keep trading until the distribution evens out and the best-day share drops below the cap. The profit stays in the account. The withdrawal waits.

That detail tells you what the rule is doing. It is not protecting the firm from a loss that already happened. It is holding back a payment until the trader proves the first number was not a fluke.

What the rule is trying to do

Strip the rule back and it is a single question asked with arithmetic: is this trader disciplined and repeatable, or did they gamble once and get lucky? A trader who makes 80% of their profit on one news spike has shown the firm nothing it can count on. A trader who grinds an even curve across 20 days has shown something repeatable. The cap is a filter for the second trader.

That is a reasonable thing to want. The firm is trying to fund behaviour, not luck. Every version of the rule, tightened or loosened or removed, is circling the same target: a disciplined trader the firm can back.

The filter works. It catches the one-lucky-day trader. It does not do the thing the operator needs.

The reframe: it measures consistency, it cannot create it

A payout gate is a detection-and-penalty mechanism. It reads the trader's history, finds the lumpy distribution, and withholds the money. Every part of that happens after the trades are closed.

The trader who is about to break the rule does not break it at payout time. They break it in the seconds before they size up after a loss, chase a position, or take the one outsized swing that makes their curve lumpy. The rule has nothing to say in that moment. It is not in the room. It speaks weeks later, as a delayed withdrawal, to a trader who has already done the thing.

The rule trains nothing. It sorts. A trader who fails it learns that they failed it, not how to become the trader who would have passed. The next cycle, the same brain meets the same trigger with the same tools, and the distribution comes out lumpy again. The firm has measured the absence of consistency without adding any.

This is the gap. Penalising inconsistency is not the same as building consistency. One sorts traders. The other changes them. The consistency rule only does the first.

Why consistency is not a setting a trader can switch on

The reason the rule cannot build what it measures sits in the trader's nervous system, not their willpower.

Consistency is discipline sustained across sessions. Discipline is not a personality trait. It is a function of the prefrontal cortex, and it is expensive, exhaustible, and slow under the conditions the rule is trying to police.

A loss large enough to register as a threat fires the amygdala before the prefrontal cortex finishes evaluating it. On LeDoux's two-route threat model the fast pathway reaches the amygdala before the cortical route has supplied context. The rational brain is not gone. It is slower than the emotional brain by a margin that decides the next click.

Two stress pathways follow. The sympathetic-adrenal-medullary axis releases adrenaline within seconds, peaking a couple of minutes in. The hypothalamic-pituitary-adrenal axis releases cortisol on a slower clock, peaking 20 to 30 minutes after the trigger. The cascade compresses the trader's time horizon, and the trader reaches for the action that resolves the threat feeling, not the one that follows the plan. That action is the revenge entry, the size-up after a loss. The behaviour that makes a profit curve lumpy is the behaviour the body produces under stress. The full neuroscience is in our earlier piece on tilt.

You cannot write a rule that reaches into that cascade. A trader sitting in a calm review reads their lumpy month and agrees they should have been steadier. The agreement is real. It is also stored in the part of the brain that goes offline the next time the trigger fires. Knowing you should be consistent and being consistent at 14:07 after a loss are two different competencies. The rule grades the first and needs the second. Education has the same blind spot, which is why an academy does not move the retention number either.

The industry is circling the same answer from two directions

Watch where the market is moving and the convergence is hard to miss. Some firms are dropping the consistency rule, calling it a payout trap that punishes good traders for one good day. Other firms are going the opposite way, building subscription models that grade traders on discipline and pay out more to the steady ones. Opposite tactics. Same belief underneath: the asset worth funding is a disciplined trader.

Both camps have found the limit of rules. Dropping the rule removes a blunt filter and builds nothing in its place. Grading discipline harder measures it with more precision and still does not teach it. The whole category now agrees on the target and is trying to hit it with measurement.

Measurement is not the missing piece. Every firm already measures. The missing piece is the layer that acts between the trigger and the trade, while the trader can still be reached.

What builds consistency

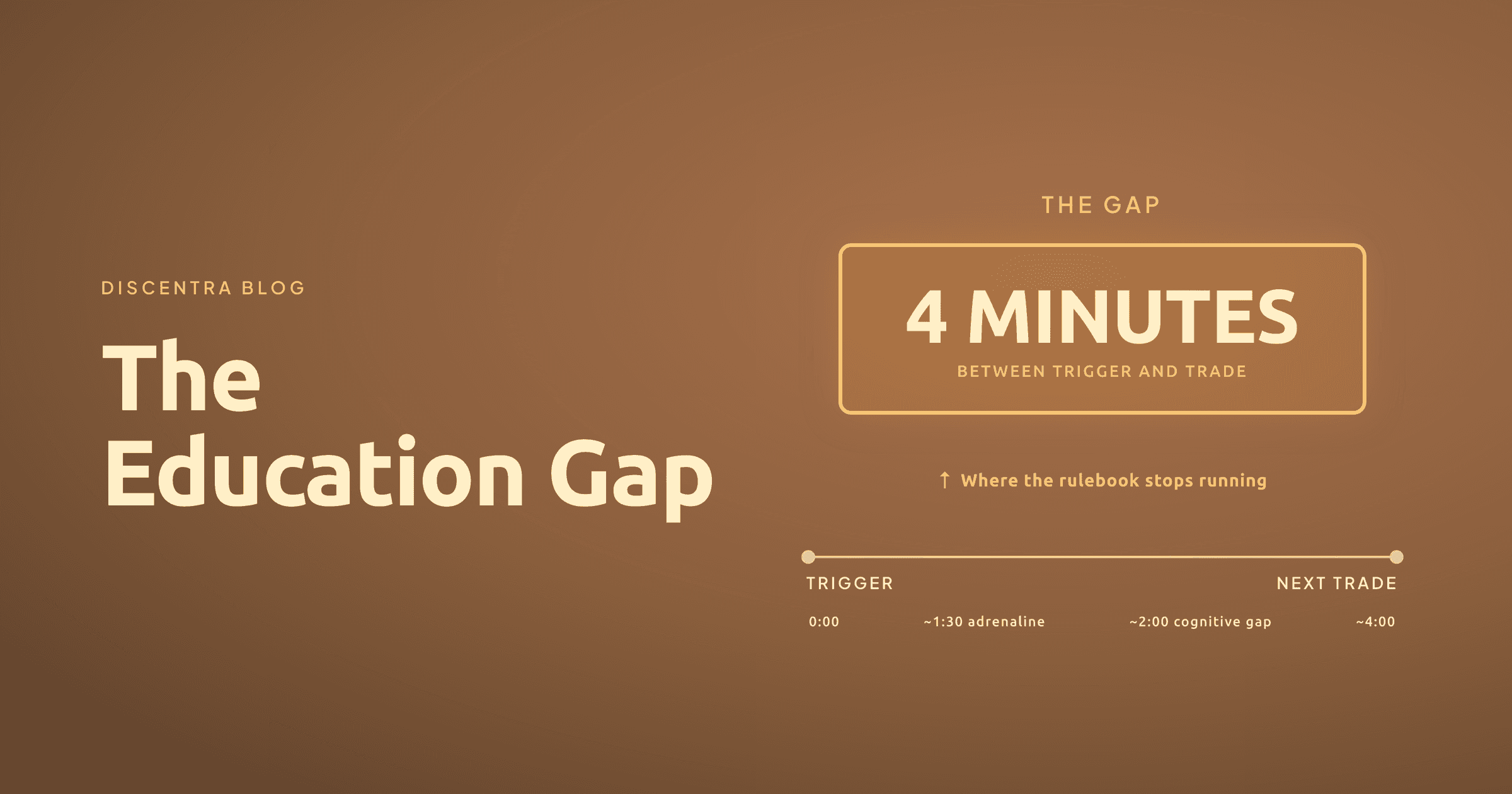

Consistency gets built in the 4 minutes the rule cannot see. The window between a trigger event and the next trade is where the lumpy day is made or avoided.

A behavioural engine watches the trading data for the signals that precede a blow-up: the revenge entry, the rapid-fire sequence, the position-size spike, the run of consecutive losses. Those patterns are visible before the breach to an engine watching in real time, and they predict churn earlier than any lagging metric. The moment one fires, the engine reaches the trader inside the window. A text nudge at the warning threshold. A voice call at active tilt. The call does what the rule cannot. It interrupts the cascade before the outsized trade, and it asks the trader what their own plan says.

That is coaching, not advice. The coach does not recommend a trade, suggest a size, or predict a price. It reflects the trader's own rules back to them at the one moment they have stopped reading them. The plan stays the trader's. The rulebook stays the trader's.

Set the two approaches side by side.

| Consistency rule | Real-time coaching | |

|---|---|---|

| When it acts | At payout, after the trades | In the 4-minute window, before the trade |

| What it does | Measures the profit distribution | Interrupts the trigger behaviour |

| Effect on the trader | Sorts pass from fail | Changes the next decision |

| Builds discipline? | No, it grades it | Yes, where it collapses |

| What the trader feels | A withheld payout | A coach in the corner |

Does this make Discentra a risk tool?

No. Discentra does not block trades, enforce the consistency rule, or make a firm compliant. It is a performance-coaching layer. The consistency rule, the daily loss limit, and the drawdown cap stay where they are. Coaching sits underneath them and does the thing none of them can. It helps the trader become the trader those rules are screening for. The rules keep sorting. The coaching changes who ends up on which side.

Three questions for your consistency rule

-

Does your consistency rule change any trader's behaviour, or only their payout date? If the only output is a delayed withdrawal, the rule is sorting, not building.

-

Does anything in your stack reach the trader in the 4 minutes when the lumpy day is made? Before the trade, not in tomorrow's report.

-

When a trader fails the rule, do they learn how to pass it next time, or only that they failed? A filter that produces no change produces the same distribution next cycle.

A consistency rule is a reasonable filter. It is necessary. It is not sufficient, because no rule reaches the trader at the moment consistency is won or lost. The firms that come through the consolidation will not be the ones with the cleverest payout gate. They will be the ones that helped the trader become consistent, so the gate had nothing to catch.

Coaching, not financial advice. The plan stays the trader's. The rulebook stays the trader's. The intervention is a coach reading that rulebook back in the 4 minutes the trader has stopped reading it themselves.

The retention case rests on numbers, not assertion. The sourced churn and CFD loss-rate figures sit here, each labelled by its source.