The quiet line in ASIC's report

In January 2026, ASIC closed a sector-wide review of contracts for difference. The headline was the refund: nearly $40 million returned to more than 38,000 retail investors after the regulator found more than half the sector had broken its product intervention order. The figure is in Australian dollars. The US-dollar equivalent sits closer to $26 million, which is why some coverage carried the smaller number.

The headline is not the part prop firm operators should read twice.

The part to read twice is what ASIC praised. Alongside the issuers that revised their target markets and rewrote their onboarding questionnaires, the regulator recorded that 42 firms "implemented new or enhanced systems to monitor client trading behaviour." That sentence moved client-behaviour monitoring from a nice-to-have to a documented regulatory expectation. The question a high-risk-product firm answers is no longer only "how did you sell this?" It is now "what did you do once you saw the client struggling?"

This piece is for operators who run a challenge-and-funding model and have read the coverage as a broker problem. It is not only a broker problem. The model the regulator is circling is the one most of the prop industry runs.

What did ASIC's CFD review find?

ASIC's Report 828, Risky business: Driving change in CFD issuers' distribution practices, reviewed 52 licensed CFD issuers between October 2024 and December 2025. The findings, in the regulator's own numbers:

- Nearly $40 million in refunds to more than 38,000 retail investors.

- More than half the sector breached the product intervention order through a margin-discount workaround.

- In the 2024 financial year, 68% of retail CFD investors lost money, totalling more than $458 million, including $73 million in fees.

- As a result of the review: 39 issuers revised their target market determinations, 46 improved website content, 44 overhauled onboarding questionnaires, and 42 built or upgraded systems to monitor client behaviour.

- The CFD product intervention order expires on 23 May 2027 unless it is remade, which puts the sector under a live clock.

ASIC Commissioner Simone Constant put it in one sentence: "Each year, thousands of Australians lose money trading CFDs and through our review we have helped put $40 million back in the pockets of more than 38,000 investors."

Why this reaches prop firms, not just brokers

ASIC reviewed CFD issuers, not prop firms. But the regulator has put the line between the two on its radar. In comments reported by Finance Magnates, Dr Rhys Bollen, who leads ASIC's Digital Assets and Markets Group, said the commission "is monitoring the emergence of 'prop trading' firms or services relating to CFD trading" and planned "detailed surveillance of new and emerging distribution methods across the CFD industry."

Read that as a category being watched, not a verdict being passed. The regulator is asking whether a model that sells repeated paid evaluations to retail traders who keep losing is a financial service or a pay-to-play structure that resembles something else. That question does not have a settled answer yet. The firms that will come through it well are the ones already operating as though the answer matters.

The direction is not Australia-specific. The UK's Consumer Duty already requires firms to evidence good outcomes for retail clients rather than assume them. European regulators publish CFD loss-rates as a standing disclosure. The common thread across jurisdictions is a shift from policing the sale to policing the outcome. A prop firm that can show what it does when a trader starts to fail is answering the question every one of these frameworks is built around.

The reframe: the question is changing

For a decade, the implicit question a prop firm answered was "how many evaluations can we sell?" The question regulators are now asking is closer to "what happens to the clients who lose?" Those are different businesses wearing the same logo.

The distinction between the two churn numbers matters here. ASIC's 68% is a loss-rate: the share of retail CFD investors who lost money in a year. Regulators publish that figure. The ~75%-quit-within-90-days number prop firms cite is churn, and it is industry-cited rather than regulator-published. The full sourcing on the churn figure is here. One number measures money lost. The other measures people leaving. They point at the same person: the trader the old model was built to replace rather than retain.

A firm cannot answer "what happens to the clients who lose?" with a discount code for the next attempt. It answers with evidence. Evidence that it saw the trader tilting, reached them before the breach, and tried to change the outcome rather than bank the next fee. That evidence does not exist unless the firm built the layer that produces it.

What "retention you can defend" looks like

Defensible retention has three properties, and they map onto the capabilities ASIC rewarded.

It monitors behaviour, not just trades. A transaction log records what happened. It does not flag the revenge entry, the rapid-fire sequence, or the position-size spike that precedes a blow-up. The six behavioural triggers that predict account failure are visible in the data before the breach, to an engine watching in real time. This is the "systems to monitor client trading behaviour" line in REP 828, built as a product rather than retrofitted under pressure.

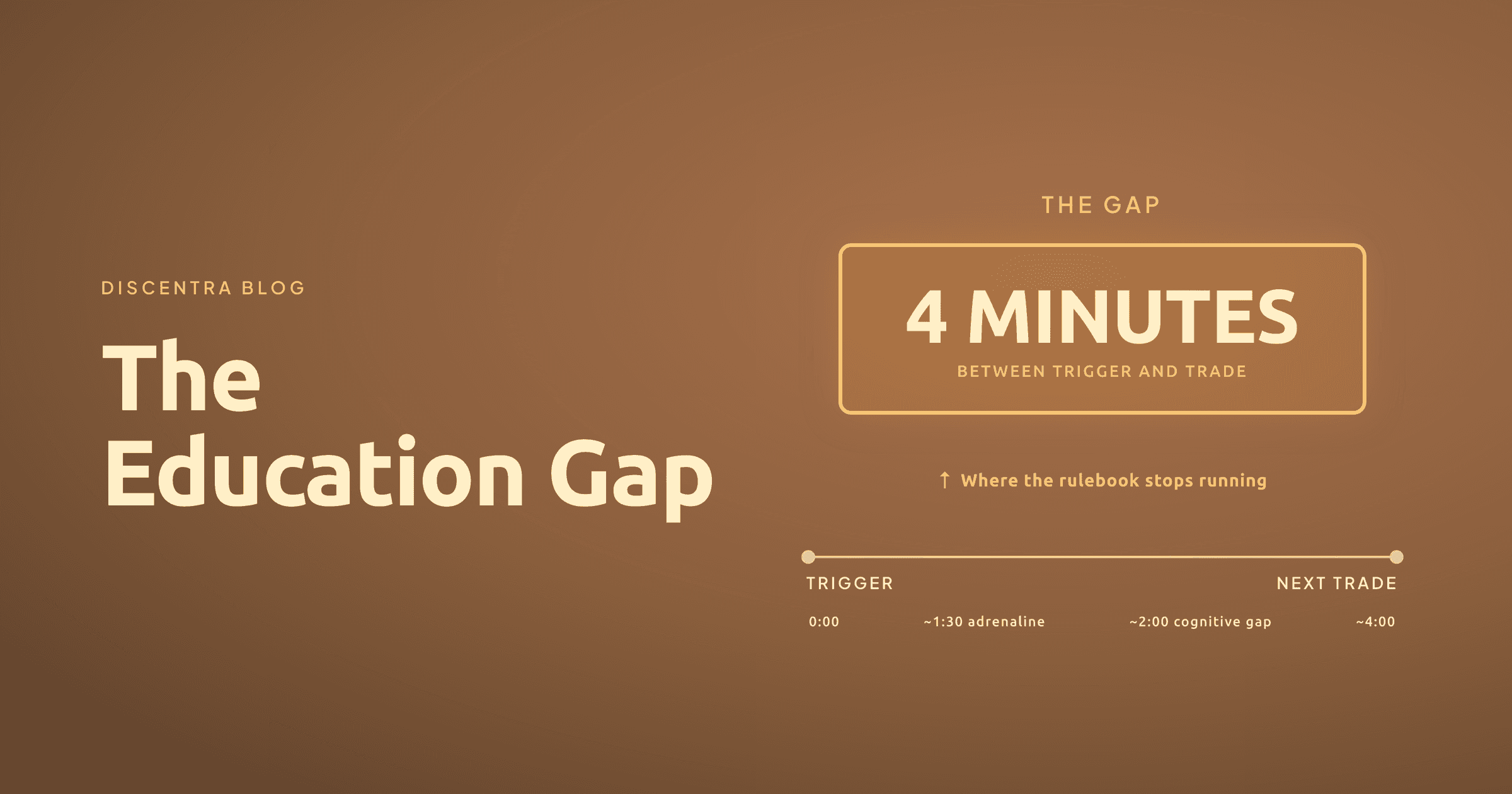

It acts inside the window. Monitoring that produces a report tomorrow is not action. The gap between a trigger event and the next trade is roughly four minutes, which is the window where discipline collapses. A text nudge at the warning threshold. A coaching call at active tilt. The intervention has to fire while the trader is still at the desk, not in the morning email.

It coaches, it does not advise. A coach asks the trader what their own plan says. It reflects the trader's rules back to them. It does not recommend trades, suggest position sizes, or predict prices. That boundary is not a disclaimer bolted on at the end. It is the difference between a layer that helps a client and a layer that creates new liability. Coaching, not financial advice.

Set the two models side by side and the regulatory exposure is hard to miss.

| Extract-and-churn | Coaching-led retention | |

|---|---|---|

| Optimises for | Evaluation fee volume | Funded-trader longevity |

| When a client struggles | Sell the next challenge | Intervene before the breach |

| What a regulator sees | Acquisition pointed at losers | Documented client-outcome monitoring |

| What the client writes | 1-star Trustpilot review | "The coaching kept me in the game" |

| How it scales | More ad spend | One engine, every funded trader |

Does this make Discentra a compliance product?

No. Discentra is a performance-coaching layer, not a compliance or risk tool. It does not block trades, file regulatory reports, or make a firm compliant. A firm's regulatory classification is the firm's own responsibility. Discentra does the thing the new question rewards: it monitors behaviour and reaches the trader at the moment discipline collapses, with coaching rather than advice. The compliance benefit is indirect, and it is real. A firm that can demonstrate it monitors client outcomes and acts on them is already answering the question regulators have started to ask.

The window is the opportunity

REP 828 reads two ways. As a cost, it is a year of retrofitting onboarding questionnaires and rewriting website disclosures to satisfy a checklist. Plenty of firms will read it that way and do the minimum.

As a signal, it is something better. The regulator has told the entire sector which capability it values: knowing what happens to the client after onboarding, and acting on it. That capability is also the one thing that moves the retention number, because the trader who blows up on a Tuesday afternoon is the same trader the regulator is counting. The retention playbook the durable firms run and the compliance posture regulators are moving toward are not two projects. They are one layer.

The firms that build it first will be able to say something their competitors cannot, to a trader and to a regulator in the same breath: we saw it coming, and we called.

Coaching, not financial advice. The plan stays the trader's. The rulebook stays the trader's. The intervention is a coach reading that rulebook back to the trader in the four minutes when they have stopped reading it themselves. That is retention you can defend.